Commodities Update - Week Ending 19 June 2022

Commodities Update - Week Ending 19 June 2022

TLDR

Ukraine continues to defend the small remainder of Sievierodonetsk but time is ticking. The Pentagon believes Putin still has his sights on most, if not all, of Ukraine.

Attention is turning to weakening demand as debilitating inflation threatens to derail the economic rebound from the pandemic-reopening. Consumer sentiment in key western economies have sunk to or are approaching record lows.

There appears to be no likely catalyst for a relief in the tight commodity complex while the eastern appears to have better chances of demand resilience as China nears an opportunity to pivot away from zero-COVID (thanks to their mRNA vaccine trials) as well as India and China’s willingness to utilize discounted Russian oil and gas.

We think East-West diffs may have legs further out the curve.

Macro Pivots

Tightening Supply

European Emergency

The conflict rages on as the Russians continue their attempt to capture the small remaining parts of Sievierodonetsk. Luhansk’s governor reported that Russia is sending a large number of reserve troops to Sievierodonetsk from other battle zones to try to gain full control of the frontline eastern city.

The Pentagon believes that while Russian President Vladimir Putin has had to narrow his tactical objectives in war (Sievierodonetsk), he likely still wants to capture much if not all of Ukraine. The Pentagon is doubtful on these ambitions being realized.

The EU continues to attempt further expansion to consolidate against Russian expansionism, backing Ukraine’s and Moldova’s membership bids. That being said, the path to actual membership of the 27-nation bloc for Ukraine and Moldova may take years as it needs reforms to conform with democratic and anti-corruption standards. Putin maintained that they have no opposition against the economic union, only against military union (NATO).

Speaking of which, NATO Secretary General Jens Stoltenberg has spoken that NATO must build out "even higher readiness" and strengthen its weapons capabilities along its eastern border in the wake of Russia's invasion of Ukraine.

Own Opinion: The recurring narratives of Russian and NATO expansion ambitions continue to support the thesis that the Russia-Ukraine war could last for years, implying persistent structural pressure on commodity supply chains until trade flows adapt to this supposed new norm.

Sanctions

With the EU having agreed on a partial embargo on Russian oil, there were no noteworthy developments regarding energy-related sanctions this week. The United States will allow certain energy-related transactions with Sberbank (SBER.MM), VTB Bank (VTBR.MM), Alfa-Bank and several other Russian entities to continue through Dec. 5, in order to allow bank transactions on Russian oil and gas sent to European countries to continue until energy sanctions fully set in. U.S. sanctions will likely correspondingly tighten by this deadline.

Russian insurers has completed the taking over of insurance coverage of Russia's state-run Sovcomflot’s cargo fleet. This will allow smoother flow of Russian exports.

Oil Flows

Russian Exports

Global crude oil loadings continued to languish at seasonal lows as companies continued to self-sanction themselves from Russian oil. Russian crude oil loadings to Europe tumbled to new seasonal lows of 2.1 mmbpd, compared to the 2016-2019 average of ~2.8 mmbpd. India and China continued to soak up Russian crude oil supply, with loadings to both countries maintaining at new seasonal highs of 1.6 mmbpd. Deputy prime minister Alexander Novak said that Russian crude output will continue to rise in July to close in on levels attained before the war in Ukraine.

OPEC

As Russian crude production continues to come under pressure, the call on OPEC beckons and the response has been disappointing with underproduction hitting new highs. Opec has slightly trimmed its forecast for this year's non-Opec supply growth, mainly on the back of a lower estimate for Russian production while keeping its demand growth projections roughly unchanged.

OPEC continues to acknowledge that there is systemic underinvestment in new oil supply globally and that it remains committed to investing in new supply.

Libyan oil output (now 100-150 kbd vs. 1,200 kbd last year) is collapsing due to the wave of shutdown of production and export facilities as a tactic in the country’s political stalemate.

Iran Sanctions

The outlook of negotiations regarding Iran nuclear sanction continue to look bleak with the US slapping on new sanctions on Iran for stonewalling the International Atomic Energy Agency, which has been investigating nuclear material found at several undeclared sites.

Gas Flows

Gas flows from Germany to France have stopped since June 15 after what German officials on Friday described as Russia's politically motivated decision to reduce supplies to the European Union. National authorities via the Gas Coordination Group claimed that there is no indication of an immediate security of supply risk.

However, Italy may declare the state of alert on gas next week if Russia continues to curb its gas supplies to Rome. The state of alert would trigger a series of measures aimed at reducing the consumption of gas, including rationing the gas to selected industrial users, ramping up the production at the country's coal power plants and also asking for more gas imports from other suppliers.

Agriculture Flows

Global food shortages continue to be key concern for policy makers. Ukraine's agriculture minister warned that Russia's invasion of Ukraine will create a global wheat shortage for at least three seasons by keeping much of the Ukrainian crop from markets, pushing prices to record levels.

Ukraine, sometimes known as Europe's bread basket, has had its maritime grain export routes blocked by Russia and faces a maelstrom of other problems, from mined wheat fields to a lack of grain storage space. Russia has also been accused of stealing grain from Ukrainian territory, with the latest shipment making its way to Syria.

U.S. President Joe Biden said on Tuesday that temporary silos would be built along the border with Ukraine in a bid to help export more grain and address a growing global food crisis. This would allow the storage of grain transported by rail to the Polish border, enabling smoother exports through Polish rail given that Ukrainian track gauges are different from those in Europe.

That being said, Black Sea shipments remain the best way to get grain exports moving again. U.N. Secretary-General Antonio Guterres is trying to broker what he calls a "package deal" to resume Ukrainian Black Sea exports and Russian food and fertilizer exports, which Moscow says had been hit by sanctions. The U.N. has so far described talks with Russia as "constructive."

Structural Fossil Fuel Shortage

Upstream

Gas

New gas deals have come through as the scramble to diversify away from Russian gas continues. The 27-nation EU, Israel and Egypt have signed a memorandum of understanding in which Israel will export natural gas in a pipeline to Egypt, where it will be turned into liquefied natural gas (LNG) then delivered to EU member states.

China's national oil majors have progressed to advanced talks with Qatar to invest in the North Field East expansion of the world's largest liquefied natural gas (LNG) project and buy the fuel under long-term contracts.

Coal

The US continued its attempt to steer back its focus towards energy security with West Virginia warning six of the nation's largest financial institutions, including JPMorgan Chase (JPM.N), BlackRock Inc (BLK.N), and Wells Fargo (WFC.N), may no longer be allowed to do business with the state of West Virginia over perceived boycotts of the fossil fuel industry. The companies will be barred from state business 45 days after the letters were sent, but have the option to appeal the decision and provide information showing they are not boycotting that particular sector.

Midstream

No noteworthy developments.

Downstream

As tensions between the Biden administration and Big Oil mount over soaring gasoline prices, U.S. Energy Secretary Jennifer Granholm called an emergency meeting with refining executives on 23 June. The meeting will "discuss steps companies can take to increase refining capacity and output and reduce gas prices in the near-term,".

In the eastern hemisphere, China's army of small, privately owned oil refiners are raising output on hopes of recovering fuel demand as COVID-19 curbs ease and refining margins swell due to an increasing supply of cheap Russian oil.

Demand Uncertainty

COVID in China

Apart from additional scares in Shenzhen and Macau, COVID in China is likely to be largely under control by now.

Movements still remain highly restrictive with lengthy quarantine times and frequent testing requirements.

Chinese mRNA

We believe that the likely catalyst for a pivot away from zero-COVID policy and therefore a meaningful resurgence in demand in the eastern hemisphere would be the approval and distribution of the home-grown mRNA vaccines.

The AWcorna vaccine, formerly known as ARCoV appears to be China’s best chance at getting a home-grown mRNA vaccine in a market dominated by inactivated vaccines. The vaccine is currently in the final stage of clinical trials. Our (very) speculative opinion is that the release of whichever home-grown vaccine that succeeds (AWcorna or SinoVac) will coincide closely with the 20th National Congress of the Chinese Communist Party a.k.a probably Q4.

Raging Inflation in the West

While a full recovery in Chinese demand would bode well for commodities, the tight commodity complex is already resulting in record high inflation which could result in a negative feedback loop into demand. Europe is hardest hit as they bear the first-degree brunt of debilitating sanctions on Russian energy.

Consumer sentiment in both the US and the EU are already at or near record lows.

In the US alone, gasoline demand remained lackluster despite the supposed summer driving season and COVID reopening narrative.

Looking Forward

Persistent inflationary forces from broad tightness in the commodity complex as well as supply chain bottlenecks threaten the economic recovery from pandemic-related reopenings.

We do not see any likely relief valve to the tight energy complex other than sanctions on Russia or Iran being lifted. The former is almost an impossibility and in fact, has the potential to be exacerbated even further if sanctions were to spread to gas flows. The latter is unlikely at best for the time being. With systemic underinvestment in exploration and production, and inflation raising the breakeven costs of new wells, we believe insufficient supply growth will continue to be structural in nature until we see a meaningful shift in CAPEX activities by producers.

As such, we believe much of the delta going forward will stem from divergences in demand. With inflation showing no signs of abating and consumer confidence tanking, demand in the back end of the curve will likely face some pressure. Meanwhile, China’s willingness to purchase cheaper Russian oil and gas as well as the availability of headroom for additional stimulus will likely mean that eastern demand will outperform western demand on a relative basis.

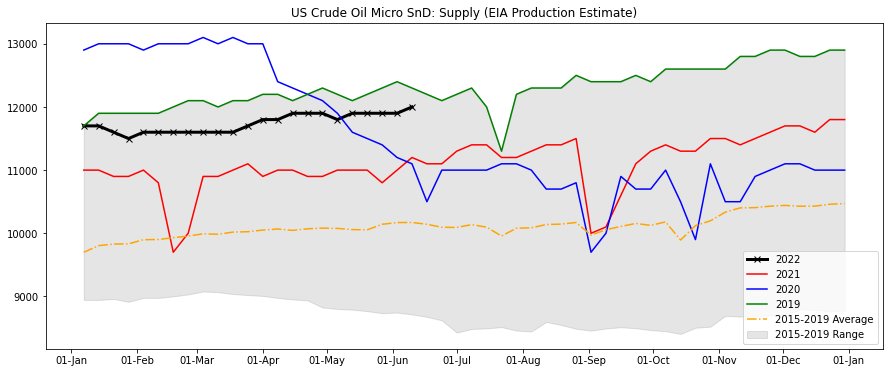

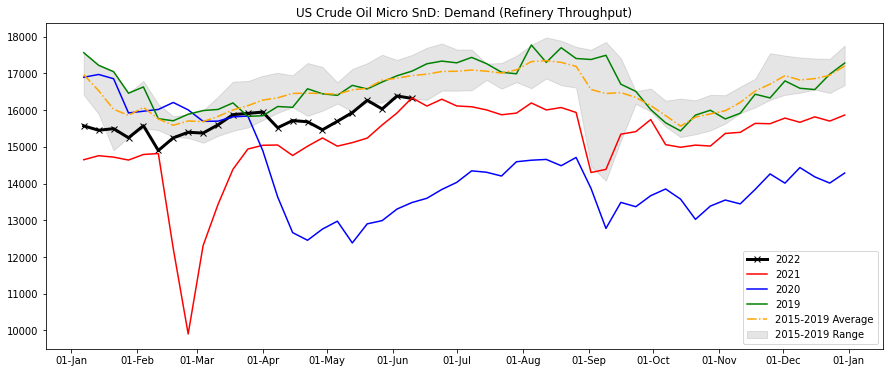

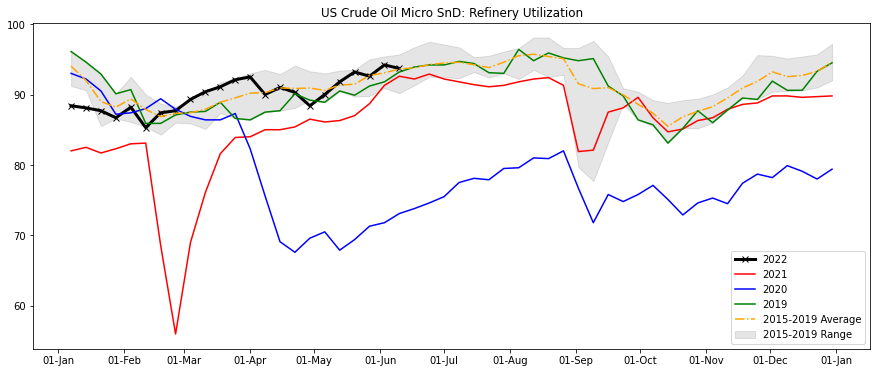

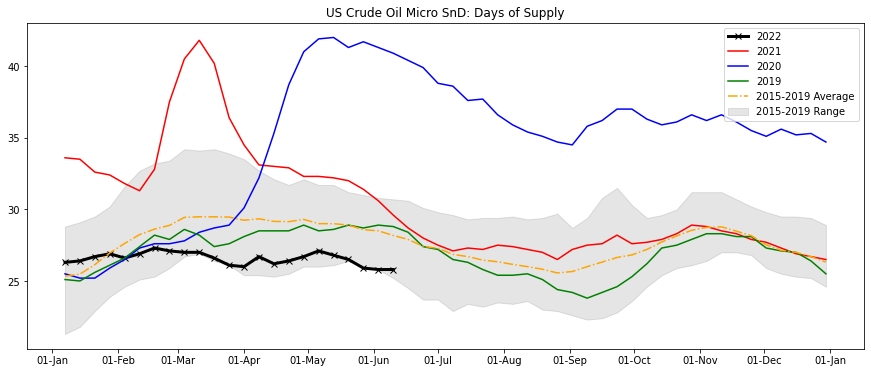

Charts